Table of Contents

ToggleWhy “Traditional” Banking Apps Are Becoming Obsolete

Neo-banking refers to digital-first financial systems that operate without traditional branch infrastructure.

Modern neo-banking is no longer defined by apps, but by a layered financial system that combines custody, settlement, yield, and compliance into a unified structure. This framework helps users and institutions understand how control, execution, and value flow within a Web3-native banking environment.

| Phase | Description |

|---|---|

| Traditional Banks | Physical + digital interfaces |

| Early Neobanks | App-based UX on legacy rails |

| Web3 Neobanks | Blockchain-native financial systems |

In 2026, neo-banking is evolving into: a programmable financial infrastructure layer

Neo-Banking is redefining how financial systems operate in 2026. Traditional banking apps, once seen as convenient, are increasingly constrained by slow settlement, limited access, and centralized control. As finance becomes global, digital, and programmable, a new model is emerging — one built on real-time settlement, self-custody, and infrastructure-native design.

The rise of Web3 neo banks signals a fundamental transition from account-based finance to wallet-based banking. Powered by blockchain, smart contracts, and Banking-as-a-Service infrastructure, these platforms offer borderless access, composability, and control that legacy banking apps simply cannot match.

This shift marks a transition from:

Many modern fintech apps still rely on traditional systems.

These platforms improve UX

but not core financial architecture

Traditional systems were designed for:

The limitation is not the interface

it is the underlying financial rails

Neo-banks look modern, but many still rely on traditional plumbing:

Golden keyword focus: SWIFT alternative blockchain

Web3 neo-banks fix this at the rails level, not just the interface.

A new category is emerging: blockchain-native financial systems.

From interface-driven finance

to infrastructure-driven finance

Settlement defines the speed and reliability of financial systems.

| Feature | Traditional Banking | Neo-Banking (Web3) |

|---|---|---|

| Settlement Time | Hours to days | Seconds |

| Availability | Limited hours | 24/7 |

| Transparency | Low | High |

| Finality | Delayed | Immediate |

Real-time settlement removes:

A hybrid financial model is emerging.

Combines:

Neo-banking expands access to financial services.

Finance becomes:

modular, accessible, and API-driven

Regulation is evolving alongside infrastructure.

Compliance is shifting from:

manual processes → code-based systems

This is the missing layer that connects everything.

| Layer | Function |

|---|---|

| Self-Custody | Asset ownership |

| Settlement | Real-time transactions |

| Yield | Capital efficiency |

| Compliance | Regulatory alignment |

This stack transforms banking into: a user-controlled financial system

Modern neo-banking is no longer defined by apps, but by a layered financial system that integrates custody, settlement, yield, and compliance into a unified structure.

Users retain direct control over assets using smart contract wallets or MPC systems, reducing reliance on centralized custody.

Blockchain-based settlement replaces legacy rails, enabling near-instant transactions and continuous availability.

On-chain identity, automated reporting, and programmable rules align financial activity with regulatory frameworks.

https://ownprocrypto.com/web3-governance-framework/

(Taxation & Reporting of Digital Assets for Investors)

Together, these layers form a sovereign finance stack, where users control assets, transactions settle instantly, and compliance is embedded into infrastructure.

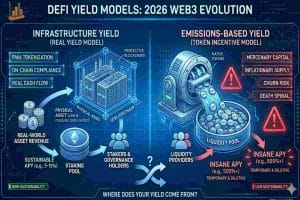

Capital can be dynamically allocated through DeFi integrations, enabling productive asset management.

https://ownprocrypto.com/digital-ownership/

(Family Office Investment Strategy post)

DeFi and fintech are finally meeting in the middle:

Golden keyword focus: DeFi fintech convergence

This is where the magic happens: speed + legality + programmability.

This is institutional-grade banking, without the legacy bottlenecks.

Transition is gradual, not immediate

hybrid systems will dominate short term

Innovation introduces efficiency

but requires informed usage

In 2026, the “Golden Rule” of banking is: If you can’t see the transaction on a block explorer, it isn’t your money. Always choose a Web3 Neo Bank that provides a transaction hash for your deposits. This ensures the bank isn’t “re-hypothecating” (lending out) your money without your knowledge.

Name: Jax, the “Yield Optimizer”

Role: Solidity Developer & DeFi Investor

The Struggle: Jax earns in stablecoins and finds it insulting to move his money into a traditional bank that pays 0.05% interest while charging him to move his own funds.

How This Post Helps: This post introduces the Yield Layer of Web3 Neo Banks, showing Jax how he can keep his money on-chain, earn 8-10% “Real Yield,” and spend it at any merchant via a Web3 Visa/Mastercard.

Name: Marcus, the “Border-Free Founder”

Role: Agency Owner with a remote team in 12 countries

The Struggle: Marcus is tired of managing 5 different currency accounts and the high “spreads” his traditional bank takes on every conversion.

How This Post Helps: He learns about the Multi-Currency Settlement Layer. This post shows him how a single Web3 Neo Bank account can act as a global hub, holding USDC but settling in local fiat (PHP, EUR, BRL) instantly at the point of sale.

Financial Infrastructure Providers

The era of app-first banking is fading; infrastructure-first is taking over.

Neo-banking is not just an evolution of apps.

It represents a shift toward:

Traditional banking systems are not disappearing immediately, but their limitations are becoming more visible in a digital-first economy.

Traditional banking apps were built for a slower, stationary world. Web3 neo banks are built for speed, mobility, and sovereignty. As finance becomes programmable and global by default, users will no longer ask which bank they belong to—but which financial stack they control. The future of banking is not an app. It’s an ecosystem you own.

Key takeaways:

Trust Links: To experience the next generation of banking, explorehttp://bleap.financefor zero-fee self-custody orhttp://revolut.comfor a hybrid fiat-crypto experience. For purely on-chain cards, check outhttp://gnosispay.com.

What are Web3 neobanks?

Web3 neobanks are blockchain-powered financial platforms that combine self-custody wallets, real-time payments, DeFi integrations, and compliant fintech services into a unified, user-owned banking experience.

What is the difference between a neobank and a Web3 neobank?

Neobanks are digital-first but still rely on traditional banking infrastructure. Web3 neobanks use blockchain for settlement, custody, and programmability—enabling real-time, borderless, and user-controlled finance.

How are Web3 neobanks different from traditional banking apps?

Traditional banking apps act as interfaces to centralized institutions. Web3 neobanks function as financial operating systems, giving users direct control over assets, programmable money flows, and global access without intermediaries.

Why are traditional banking apps becoming obsolete?

They are slow, geographically restricted, and operationally rigid. As demand grows for instant settlement, global access, and financial sovereignty, legacy systems struggle to compete with real-time, borderless alternatives.

How do Web3 neobanks make money?

They generate revenue through transaction fees, fiat–crypto spreads, subscription tiers, lending services, and integrations with DeFi protocols. Some also monetize via embedded finance and API-based services.

Are Web3 neobanks regulated?

Yes. Many operate within regulated frameworks using Banking-as-a-Service (BaaS), while leveraging blockchain for settlement, custody, and payments—blending compliance with decentralization.

Are Web3 neobanks safe to use?

Security is built into the architecture through smart contracts, cryptographic verification, multi-signature authorization, and audited infrastructure. However, safety depends on implementation quality and user practices.

Are Web3 neobanks insured like traditional banks?

Not in the traditional sense. Instead of deposit insurance, they rely on mechanisms like smart contract insurance, over-collateralization, and proof-of-reserve transparency to reduce systemic risk.

Do Web3 neobanks require KYC?

Most compliant platforms require KYC for fiat on/off-ramps and regulated services, while some DeFi features may remain permissionless depending on jurisdiction.

What risks are unique to Web3 neobanks?

Key risks include smart contract vulnerabilities, regulatory uncertainty, and user-side risks like private key management—though transparency can reduce hidden systemic risks.

Can I pay everyday bills with a Web3 neobank?

Yes. Many offer virtual IBANs or similar banking bridges, enabling payments (rent, utilities) via traditional rails like SEPA or ACH directly from digital asset balances.

Do Web3 neobanks support cross-border payments?

Yes. Using blockchain rails and stablecoins, they enable near-instant global transfers with significantly lower fees than traditional banking systems.

How do Web3 neobanks handle custody?

They typically use hybrid models: self-custody wallets for user control, institutional-grade custody for security, and optional recovery mechanisms for usability.

What role do stablecoins play in Web3 neobanks?

Stablecoins power instant, low-cost transactions and serve as the foundation for real-time settlement, cross-border transfers, and programmable financial workflows.

Do Web3 neobanks replace DeFi platforms?

No. They act as bridges—integrating DeFi, stablecoins, and traditional financial rails into one seamless interface.

What is real-time settlement in Web3 banking?

It means transactions are finalized instantly on-chain without intermediaries, making funds available immediately—unlike traditional systems that take hours or days.

What is a bank-backed token?

A bank-backed token is a digital representation of fiat issued or supported by a regulated institution, combining stability with blockchain speed and programmability.

What is Banking-as-a-Service (BaaS) in Web3?

BaaS enables Web3 platforms to integrate regulated financial services (IBANs, cards, fiat access) via APIs, combining compliance with blockchain infrastructure.

What is programmable finance?

Programmable finance uses smart contracts to automate financial actions—such as payments, compliance checks, and treasury management—without manual intervention.

What is the role of AI in Web3 neobanks?

AI is used for fraud detection, risk analysis, automation, and personalized financial insights—becoming a key intelligence layer in modern financial systems.

Can Web3 neobanks replace traditional banks completely?

Not yet. While they offer speed, control, and global access, traditional banks still dominate lending, regulation, and institutional trust. The near-term future is hybrid.

Welcome to OwnProCrypto (Own & Pro Crypto) — a next-generation Bitcoin and blockchain education platform where the science of finance meets the power of AI-driven automation.

Our mission is simple: to equip you with the knowledge, frameworks, and tools needed to make smarter financial and business decisions in the Web3 economy.

Beyond analysis, OwnProCrypto focuses on transparency, verifiable data, and practical frameworks that investors and builders can actually use. Our goal is not hype — but clear thinking, disciplined analysis, and long-term value creation in the decentralized economy.

Our Background: Salim (Sam) is the founder and lead researcher behind OwnProCrypto, a Web3 intelligence platform focused on crypto security, digital ownership, stablecoin systems, interoperability, and institutional blockchain infrastructure.

Crypto Tools & Analysis:

Crypto Fundamental Analysis Tool | Protocol Evaluation System | DeFi Risk Analysis Tools | Crypto Portfolio Dashboard | Token Risk vs Reward Tool

Guides:

Crypto Fundamental Analysis | Blockchain Project Evaluation | Tokenomics Analysis | DeFi Protocol Analysis | Capital Efficiency

© 2026 OwnProCrypto — Built for smarter crypto decisions