Table of Contents

ToggleCross-border payments are still stuck in the past. Traditional systems rely on intermediaries, delayed settlement, and opaque fees. Sending money internationally can take 2–5 days and cost up to 5% in fees.

Stablecoin payments change that.

They enable near-instant settlement, transparent fees, and global access—without relying on legacy infrastructure like SWIFT. But there’s a catch: one mistake in execution can result in permanent loss of funds.

This guide explains how stablecoin payments work, compares them with traditional systems, and introduces a safe way to practice before going live.

Stablecoin payments use digital assets (like USDC or USDT) pegged to fiat currencies to transfer value globally.

Unlike volatile cryptocurrencies, stablecoins maintain a relatively stable price, making them suitable for payments, remittances, and business transactions.

Key Characteristics

At a high level, every stablecoin payment follows four stages:

Legacy systems weren’t designed for real-time global commerce.

| Problem | Traditional Systems |

|---|---|

| Settlement Time | 2–5 days |

| Fees | 3–5% |

| Transparency | Low |

| Intermediaries | Multiple banks |

| Reversibility | Limited |

These inefficiencies create friction for freelancers, startups, and global businesses.

Here’s where stablecoins fundamentally change the game:

| Feature | Stablecoins | Traditional (SWIFT) |

|---|---|---|

| Speed | Seconds | Days |

| Cost | Low ($1–$5) | High (%) |

| Transparency | High | Low |

| Availability | 24/7 | Banking hours |

| Settlement Finality | Instant | Delayed |

This is why companies like Stripe and Crossmint are moving toward stablecoin infrastructure.

A real system isn’t just a wallet—it’s a stack of services working together:

This is what turns a simple transfer into a reliable financial operation.

Before using stablecoins, you must understand the risks.

Unlike banks, there’s no “undo” button.

Smart contracts play a vital role in stablecoin security. Auditing the smart contract architecture ensures that minting, pausing, and transferring logic remains secure against exploits

| Audit Area | What to Verify | Why It Matters in 2026 |

|---|---|---|

| Smart Contract Architecture | Use of proxy patterns, emergency pause functions, and multi-sig or DAO-controlled minting | Prevents unilateral minting or irreversible contract exploits |

| Wallet Management | Account abstraction, spending limits, social recovery | Eliminates single-seed failure and improves enterprise custody |

| On-Chain Monitoring | Real-time alerts for large transfers, blacklist enforcement (OFAC / Chainalysis) | Reduces compliance and sanctions exposure |

| Compliance Automation | Auto KYC/KYB refresh for transactions above $10,000 | Aligns with 2026 AML and payment-rail mandates |

| Custody Segregation | Separation of operational funds and customer reserves | Protects users during issuer or custodian insolvency |

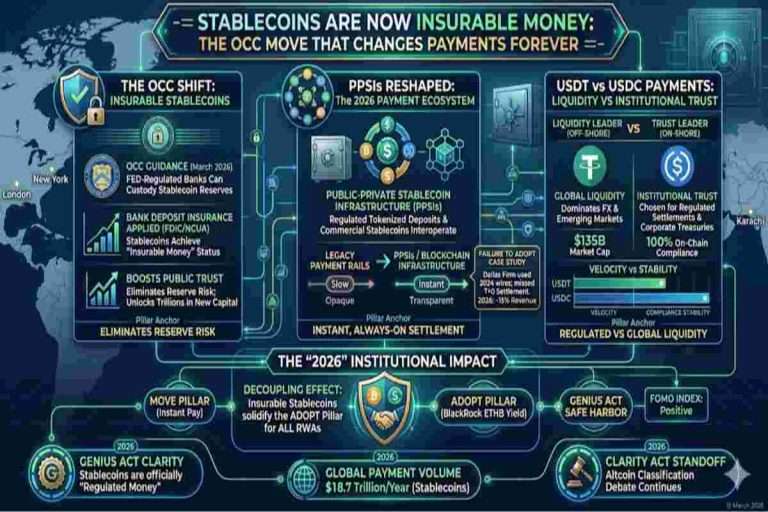

Competition from new regulated stablecoins is rising — but dethroning USDT and USDC requires matching liquidity, trust, and network effects simultaneously.

This is where your tool becomes powerful.

Instead of risking real money, users can simulate the entire payment flow.

Think of it as a flight simulator for financial infrastructure

Client

│

▼

API Gateway

│

▼

Payment Service ───────► Compliance

│ │

│ ▼

│ Approved

▼

Routing Engine

│

▼

Onramp ──► Wallet ──► Blockchain ──► Offramp

│ │

└──────────────► Ledger ◄──────────────┘

│

▼

Notification

Your platform acts as the coordination layer between systems.

Let’s simulate a real transaction:

| Step | Action |

|---|---|

| Input | 1000 USD |

| Conversion | USDC → AEDC |

| Routing | Select cheapest chain |

| Transfer | Blockchain execution |

| Output | AED in recipient bank account |

| Metric | Value |

|---|---|

| Settlement Time | ~5 seconds |

| Fee | ~$2–$3 |

| Chain Used | Solana / Stellar |

Different blockchains offer different trade-offs:

| Blockchain | Avg Fee | Speed | Strength |

|---|---|---|---|

| Ethereum | High | Medium | Liquidity |

| Solana | Low | Fast | Cost efficiency |

| Stellar | Very Low | Very Fast | Payments focus |

Choosing the right chain is where routing engines add value.

Safety depends on implementation.

While adoption is growing, regulations differ globally—always verify local laws before deploying at scale.

This table highlights why enterprises are switching to on-chain rails.

| Metric | Traditional Cross-Border (SWIFT) | Stablecoin Settlement (L2/Solana) |

| Settlement Time | 3 – 5 Business Days | 2 – 5 Minutes (T+0) |

| Avg. Transaction Fee | $25 – $50 + 3% FX Spread | <$0.01 – $1.00 (Flat) |

| Network Availability | Banking Hours (Mon–Fri) | 24 / 7 / 365 |

| Intermediaries | 3 – 5 Correspondent Banks | 0 (Peer-to-Peer) |

| Failure Rate | ~2% – 5% (Data Errors) | <0.1% (On-chain Validation) |

Stablecoins are not just for crypto users.

The key personas driving adoption include the Global Merchant, the Institutional Treasurer, and the Remittance Worker, each utilizing stablecoins to solve specific financial pain points.

In Stablecoin Payments 2026 four distinct personas have emerged as the primary drivers of on-chain volume, each selecting their “digital dollar” based on specific needs for On-Chain Compliance and Capital Efficiency.

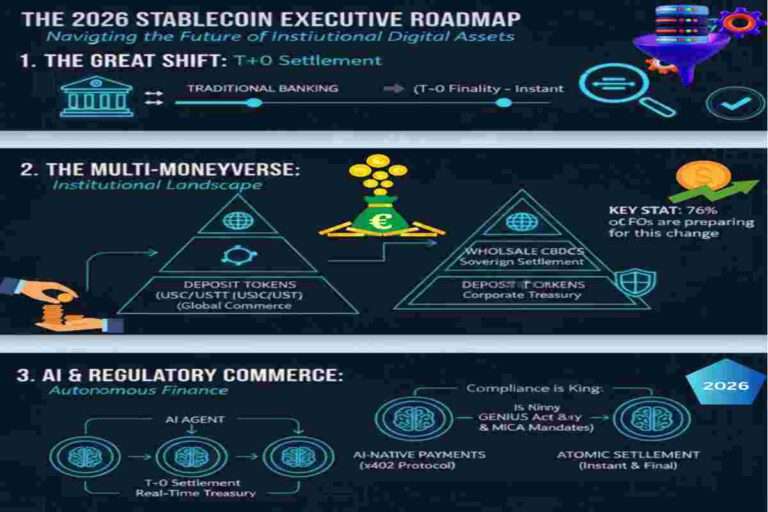

Stablecoin payments in 2026 should be treated as core financial infrastructure, not speculative exposure. Use USDC for regulated treasury management and audited reporting, and USDT for global liquidity and emerging-market reach.

Prioritize platforms with strong on-chain compliance, transparent reserves, and multi-chain support. When integrated correctly, stablecoin payments become a competitive advantage—unlocking capital efficiency, real yield, and jurisdictional resilience.

Stablecoins are evolving into core financial infrastructure.

To secure your Stablecoin Payments & Finance 2026 market shifts, you need more than just theory—you need execution. We have developed the complete Digital Sovereignty Tool & Pillar Template Set, designed specifically for institutional-grade asset management and on-chain succession planning. This toolkit includes the RWA S-Curve Projection Model, the Smart Contract Will Framework, and the Capital Efficiency Audit.

Stablecoin Payments & Finance (11 sheets)

Purpose: Evaluate stablecoin networks, payments, and adoption metrics.

What is a stablecoin payment 2026?

A stablecoin payment is a digital transaction using cryptocurrencies pegged to fiat currencies (like USD). It allows users to send money globally with minimal volatility and near-instant settlement.

How do stablecoin payments work step by step?

Stablecoin payments follow four main steps: converting fiat into stablecoins (onramp), selecting the best blockchain (routing), transferring funds via blockchain, and converting back to local currency (offramp).

Do I need a crypto wallet to use stablecoins?

Yes, most stablecoin transactions require a wallet. However, modern platforms and APIs can abstract this layer, allowing users to send payments without directly managing private keys.

Are stablecoin payments cheaper than bank transfers?

Yes. Stablecoin payments typically cost between $1–$5 depending on the blockchain, while traditional bank transfers can charge 3–5% in fees plus hidden FX costs.

How fast are stablecoin transactions?

Most stablecoin transactions settle within seconds to a few minutes, depending on the blockchain network used.

What affects stablecoin transaction fees?

Fees depend on the blockchain (Ethereum vs Solana vs Stellar), network congestion, and routing decisions made by the payment system.

Can I reverse a stablecoin transaction?

No. Stablecoin transactions are irreversible once confirmed on the blockchain. This is why accuracy in wallet addresses and network selection is critical.

What happens if I send funds to the wrong address?

Funds are usually lost permanently. There is no central authority to recover them, which is why practicing in a simulation environment is highly recommended.

Are stablecoin payments safe?

They are generally safe when using trusted platforms and secure wallets, but risks include user error, smart contract vulnerabilities, and regulatory uncertainty.

Can I send money internationally using stablecoins?

Yes. Stablecoins are widely used for cross-border payments because they bypass traditional banking delays and reduce fees significantly.

Which stablecoin is best for payments?

Popular options include USDC and USDT due to their liquidity and widespread support across exchanges and payment platforms.

Are stablecoins legal in all countries?

No. Regulations vary by country. Some regions fully support stablecoins, while others restrict or regulate their usage. Always check local laws before using them.

What is a stablecoin payment API?

A stablecoin payment API allows developers to integrate sending, receiving, and managing stablecoin transactions into apps or platforms programmatically.

How do companies integrate stablecoin payments?

Companies use infrastructure providers like Stripe or Crossmint, or build orchestration layers that connect wallets, blockchains, and banking systems.

What is a stablecoin orchestration layer?

It is a system that coordinates the entire payment flow—onramp, routing, blockchain transfer, and offramp—through a single unified API.

Can I test stablecoin payments without real money?

Yes. Simulation tools allow users to practice the full payment flow without financial risk, helping them understand routing, fees, and transaction steps safely.

Why should I practice before using real stablecoins?

Because mistakes in real transactions are irreversible. Practicing helps you understand the process, avoid errors, and gain confidence before handling real funds.

Stablecoin payments unlock faster settlement, global accessibility, and programmable finance — but they also come with very little room for error. A wrong wallet address, incorrect network selection, or failed routing decision can result in irreversible loss of funds. In a system where transactions move instantly and without intermediaries, preparation becomes just as important as execution.

That is why simulation and hands-on practice matter before using real capital. The Stablecoin Payment 2026 Simulator provides a controlled environment where users can safely explore how modern digital payment infrastructure works without financial risk. Your Stablecoin Orchestration Layer helps users understand transaction flows, payment routing, settlement logic, and operational behavior in a practical way rather than just theoretical learning.

By practicing first, users can build familiarity, reduce mistakes, and gain confidence before moving into live transactions. The goal is not only to learn stablecoin payments, but to understand how the next generation of digital financial systems will actually operate in the real world.

Practice here first. Execute with confidence later.

U.S. Treasury Digital Asset Report — Official insights into stablecoins, regulation, and the future of digital money. U.S. Treasury Digital Asset Report

Welcome to OwnProCrypto (Own & Pro Crypto) — a next-generation Bitcoin and blockchain education platform where the science of finance meets the power of AI-driven automation.

Our mission is simple: to equip you with the knowledge, frameworks, and tools needed to make smarter financial and business decisions in the Web3 economy.

Beyond analysis, OwnProCrypto focuses on transparency, verifiable data, and practical frameworks that investors and builders can actually use. Our goal is not hype — but clear thinking, disciplined analysis, and long-term value creation in the decentralized economy.

Our Background: Salim (Sam) is the founder and lead researcher behind OwnProCrypto, a Web3 intelligence platform focused on crypto security, digital ownership, stablecoin systems, interoperability, and institutional blockchain infrastructure.

Crypto Tools & Analysis:

Crypto Fundamental Analysis Tool | Protocol Evaluation System | DeFi Risk Analysis Tools | Crypto Portfolio Dashboard | Token Risk vs Reward Tool

Guides:

Crypto Fundamental Analysis | Blockchain Project Evaluation | Tokenomics Analysis | DeFi Protocol Analysis | Capital Efficiency

© 2026 OwnProCrypto — Built for smarter crypto decisions