Table of Contents

ToggleStablecoins have evolved from trading instruments into global settlement infrastructure. Today they are used for remittances, treasury operations, cross-border commerce, and enterprise settlement.

Stablecoins are becoming a key part of how money moves across the world. What started as a crypto tool is now turning into real payment infrastructure for businesses, helping move value across borders in a faster and more reliable way. In 2026, more companies and institutions are using stablecoins for things like cross-border payments, remittances, treasury operations, and managing liquidity. Instead of waiting on slow banking systems, they are starting to use always-on digital settlement networks that work around the clock.

This shift is not just about new technology, it is about a better way to move money globally. Stablecoin systems are making payments faster, more predictable, and easier to connect across countries. At the same time, regulators and financial institutions are starting to set clear rules around how these systems should work. As adoption grows, stablecoins are quietly becoming part of the core infrastructure behind global finance, built for speed, simplicity, and continuous cross-border movement.

This hub explains how stablecoin payments work, why adoption is accelerating, and how businesses, investors, and institutions are preparing for the next phase of digital finance.

Most people still associate stablecoins with cryptocurrency trading.

In reality, stablecoins have become a global settlement layer.

The industry is rapidly shifting from speculative use cases toward operational use cases:

Traditional System | Stablecoin System |

Banking Hours | 24/7 |

Multiple Intermediaries | Direct Settlement |

High FX Costs | Lower Transfer Costs |

Slow Cross-Border Transfers | Near Real-Time Transfers |

Limited Accessibility | Global Accessibility |

The purpose of this hub is to help readers understand this transformation from both a user and institutional perspective.

Stablecoin payments work like a connected flow of financial steps.

Money does not move in one jump — it moves through a structured system.

Fiat Money (USD, EUR, etc.)

↓

Exchange / On-Ramp System

↓

Stablecoins (USDT / USDC issued or converted)

↓

Blockchain Network (Settlement Layer)

↓

Wallets / APIs / Payment Systems

↓

Merchant / Business / Treasury

↓

Final Settlement Recorded On-ChainHow to understand this simply:

This removes delays and reduces dependency on traditional banking systems.

Stablecoin payments are not a single product. They are a full financial system made of different layers working together.

This is the base system that moves money:

This layer controls value flow:

This layer ensures compliance and trust:

This is where real-world adoption happens:

Stablecoins are not growing because of hype.

They are growing because they solve real problems.

Here is what is changing in real life:

The biggest change is this:

Payments are no longer limited by banking hours or borders.

Money now moves continuously.

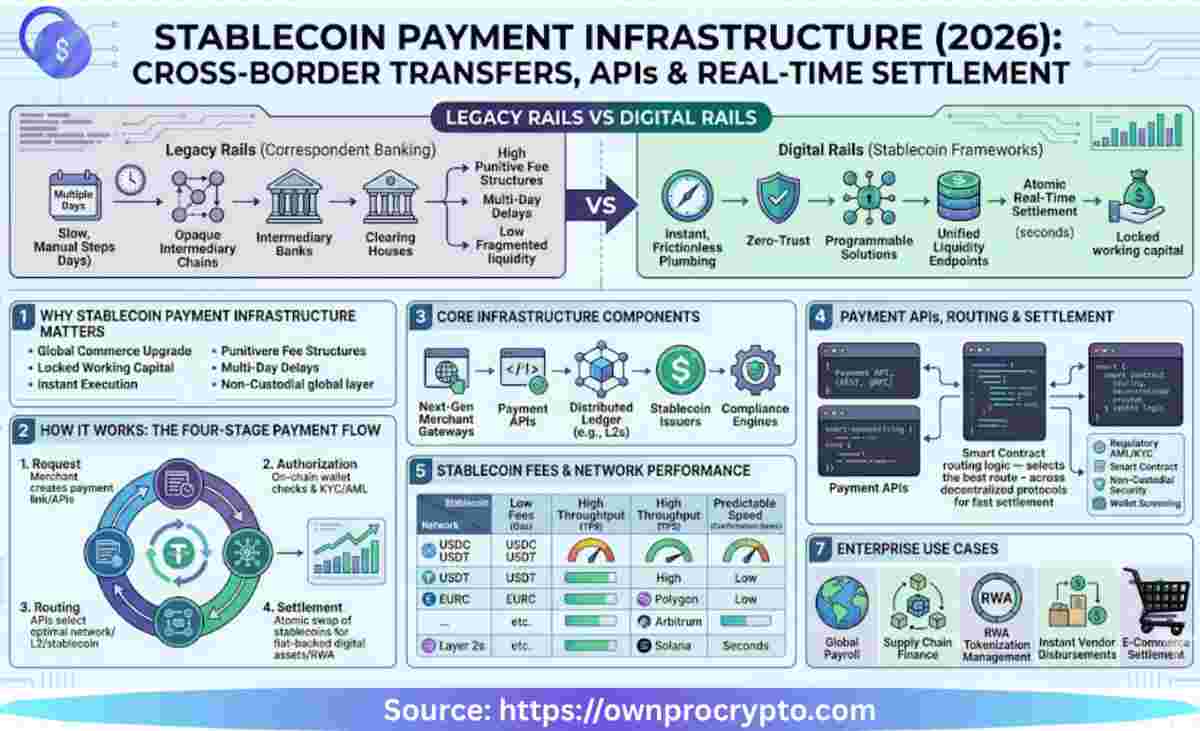

Stablecoins are increasingly being used as global settlement networks that move value across borders without relying on traditional banking hours or correspondent banking chains. These networks support real-time transfers, continuous settlement, and greater accessibility for businesses, institutions, and individuals participating in the digital economy.

Cross-border payments are one of the largest use cases for stablecoins. By reducing settlement delays and intermediary costs, stablecoin networks enable faster movement of funds between countries.

Merchants can use stablecoins to accept and settle payments without waiting for traditional banking processes. This can improve cash flow and reduce transaction friction.

Organizations are increasingly using stablecoins to move capital between accounts, subsidiaries, and business units. Treasury settlement can occur continuously rather than during limited banking windows.

Businesses use stablecoins to settle invoices, supplier payments, and commercial transactions more efficiently across jurisdictions.

In regions with limited banking access or currency instability, stablecoins are becoming an alternative settlement tool for commerce, savings, and international payments.

Every major financial shift creates tension.

Stablecoin payments are part of a global financial transition, and that creates competition between systems.

Key conflicts include:

These conflicts are shaping the future of global finance, which is why this topic is gaining strong attention in search and markets.

Stablecoin payments don’t rely on banks, clearing houses, or correspondent networks. Instead, they move on blockchain rails like:

A transaction settles in seconds (sometimes milliseconds), operates 24/7, and can be verified on-chain. This architecture explains why stablecoin payments are faster than SWIFT or wire transfers and why they’re increasingly used for cross-border settlement.

With a combined market capitalization exceeding $260 billion, USDT and USDC now settle more value daily than traditional card networks. This is a structural signal, not a temporary spike.

Stablecoins have crossed the threshold from alternative payment method to core financial infrastructure, supporting retail payments, enterprise settlement, and cross-border trade simultaneously.

Not every payment needs stablecoins, and not every system needs banks.

Here is a simple way to decide:

| Use Case | Best Option |

|---|---|

| Cross-border payments | Stablecoins |

| Freelancer / contractor payments | Stablecoins |

| Internal treasury transfers | Stablecoins |

| Compliance-heavy institutional transfers | Traditional banking |

| High-risk trading environments | Crypto exchanges |

This helps businesses choose the right system instead of using one approach for everything.

User | Primary Benefit |

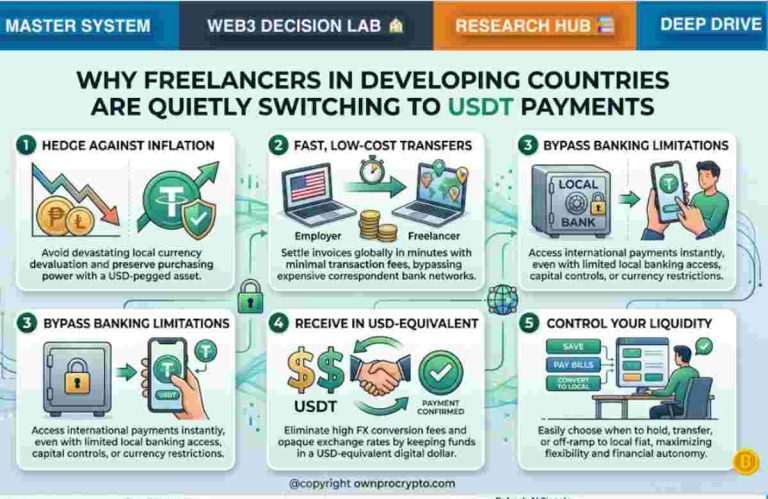

Freelancer | Faster international payments |

Merchant | Lower payment processing costs |

Startup | Global treasury management |

Enterprise | Faster settlement |

Institution | Liquidity management |

Government | Digital payment infrastructure |

Reserve Assets

↓

Custody Protection

↓

Independent Audits

↓

Regulatory Compliance

↓

Insurance Protection

↓

Institutional Adoption

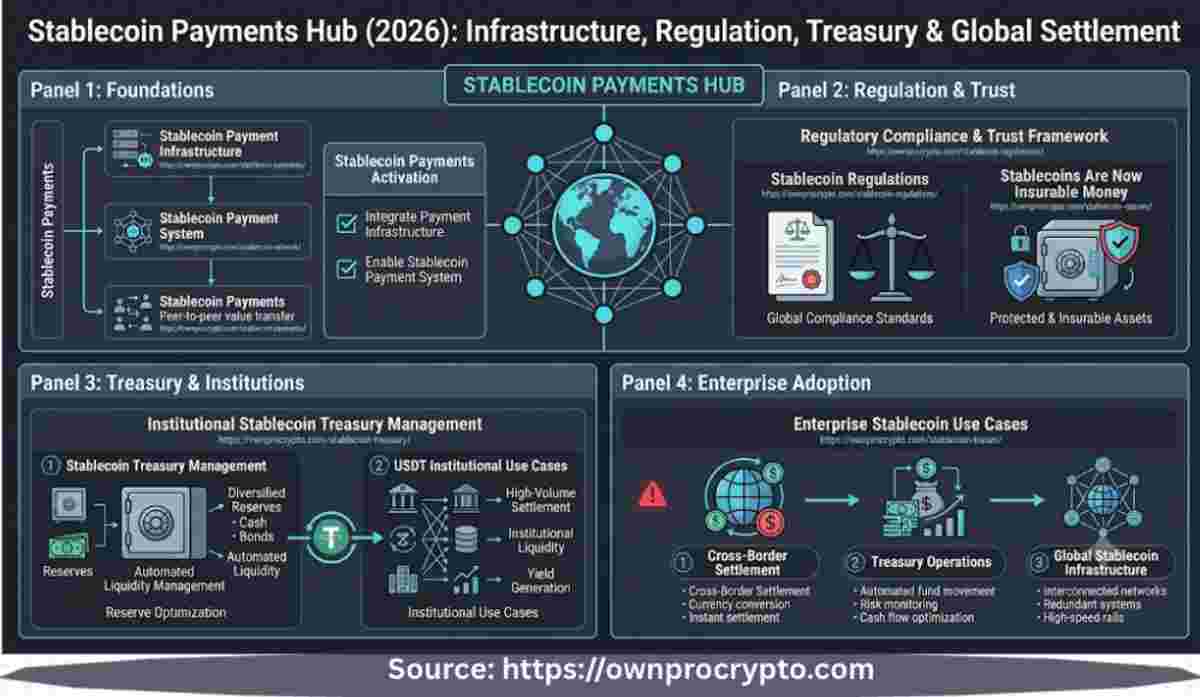

The stablecoin payments ecosystem consists of multiple participants working together to facilitate issuance, custody, settlement, compliance, and payment processing. Understanding these stakeholders helps explain how stablecoin transactions operate at scale.

Issuers create and manage stablecoins while maintaining the reserves that support their value.

Payment providers connect businesses and users to stablecoin payment networks through APIs, gateways, and settlement services.

Custodians secure digital assets and help institutions manage stablecoin holdings in a compliant manner.

Banks are increasingly exploring partnerships and infrastructure that support stablecoin-related services and settlement activities.

Enterprises use stablecoins for payments, treasury management, liquidity optimization, and international operations.

Regulators establish the legal frameworks that govern issuance, custody, settlement, reporting, and consumer protection.

If you want to understand how stablecoin payments actually work in real-world finance, these focused learning paths break the system into deeper layers—covering infrastructure, regulation, treasury operations, institutional usage, and trust frameworks.

Stablecoin payments rely on a full technical stack that includes blockchain networks, wallet systems, payment APIs, routing layers, and settlement infrastructure. This layer explains how value actually moves across global digital rails in real time.

Read Next: Stablecoin Payment Infrastructure Guide

👉 https://ownprocrypto.com/stablecoin-payment-infrastructure/

Beyond infrastructure, stablecoin payment systems define how transactions are initiated, processed, verified, and settled across networks. This includes real-time payment flows, cross-border execution, and merchant-level integration.

Read Next: Stablecoin Payment System Overview

👉 https://ownprocrypto.com/stablecoin-payment-system/

Regulation defines the boundaries of stablecoin adoption. This includes reserve requirements, licensing frameworks, compliance rules, audit standards, and emerging global policies shaping how digital money operates legally.

Read Next: Stablecoin Regulatory Framework (2026)

👉 https://ownprocrypto.com/stablecoin-regulations/

Stablecoins are increasingly evaluated through institutional trust frameworks that include reserves, custody models, third-party audits, regulatory supervision, and insurance protection layers.

Read Next: Stablecoin Trust & Risk Model

👉 https://ownprocrypto.com/stablecoins-are-now-insurable-money/

Treasury systems use stablecoins for liquidity allocation, cross-border cash flow control, yield strategies, and real-time capital movement across wallets and institutions.

Read Next: Stablecoin Treasury Operations Guide

👉 https://ownprocrypto.com/stablecoin-treasury/

USDT plays a major role in global liquidity flows, including cross-border payments, treasury settlement, contractor payouts, and institutional capital movement where speed and accessibility matter most.

Read Next: USDT Institutional Adoption Explained

👉 https://ownprocrypto.com/usdt-institutional-use-cases/

These templates are used to track, manage, and understand stablecoin operations in real scenarios.

| Wallet / Account | Opening Balance | Inflows | Outflows | Current Balance | Allocation % | Yield Strategy | Risk Level |

|---|---|---|---|---|---|---|---|

| Wallet A (USD) | |||||||

| Wallet B (USDC) | |||||||

| Exchange Account | |||||||

| Total | 100% |

Purpose:

Helps track stablecoin liquidity across wallets and allocate funds efficiently for operations, yield, and risk control.

| Transaction ID | Sender | Receiver | Amount | Token Type | Network | Fee | Status | Settlement Time |

|---|---|---|---|---|---|---|---|---|

Purpose:

Tracks how money moves across blockchain networks in real time, especially for cross-border or business payments.

| Asset | Network | Exposure % | Custody Type | Risk Level | Action |

|---|---|---|---|---|---|

| USDT | Tron | Wallet / CEX | Medium | Monitor |

Purpose:

Helps identify where funds are exposed and what risk level each asset carries.

| Region | Regulation Status | KYC Level | Reporting | Risk Level |

|---|---|---|---|---|

| USA | Active | High | Monthly | Low |

Purpose:

Helps ensure legal and regulatory alignment for stablecoin operations.

| Organization Type | Use Case | Stage | Volume | Risk Level |

|---|---|---|---|---|

| Fintech | Payments | Pilot | Medium |

Purpose:

Tracks how institutions and businesses are adopting stablecoin systems over time.

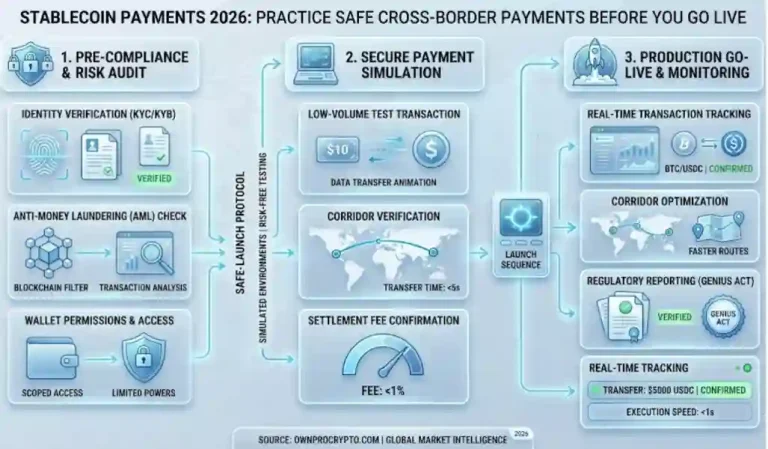

Stablecoin payments offer significant advantages in speed, accessibility, and operational efficiency. However, organizations must also consider regulatory, operational, and counterparty risks when implementing stablecoin-based payment systems.

Stablecoins can reduce settlement times, lower transaction costs, improve liquidity management, and enable global payments that operate around the clock.

Potential risks include regulatory uncertainty, reserve management concerns, operational failures, cybersecurity threats, and issuer-related risks.

Organizations can reduce risk through compliance programs, diversified custody arrangements, transaction monitoring, and strong treasury controls.

Stablecoin adoption continues to expand as financial institutions, payment providers, and regulators build the infrastructure needed for broader integration. While the market remains in a period of evolution, stablecoins are increasingly positioned as a foundational component of modern global payment systems.

Stablecoin payments are no longer just a crypto use case—they are becoming a parallel financial system.

What is happening in 2026 is not an upgrade of banking. It is a shift in how money moves entirely. Traditional systems were built around delayed settlement, intermediaries, and limited operating hours. Stablecoin rails remove those constraints and replace them with continuous, programmable settlement networks.

This does not mean banks disappear. It means financial flows split into two systems:

Over time, businesses, fintechs, and even institutions are likely to use both—depending on cost, compliance, and speed requirements.

The direction is clear: money is becoming software-driven, always-on, and globally interoperable.

STABLECOIN PAYMENTS HUB

├── Foundations

├── Stablecoins Are Now Insurable Money

├── Regulation & Trust

└── Stablecoins Are Now Insurable Money

├── Treasury & Institutions

├── Stablecoin Treasury Management

└── USDT Institutional Use Cases

└── Enterprise Adoption

Stablecoin payments are used for cross-border transfers, treasury management, freelancer payments, and fast global settlements without relying on traditional banking delays.

Not fully. Banks still handle compliance-heavy and regulated financial activity, but stablecoins are increasingly used for fast settlement and global transfers.

USDT is widely used for liquidity and global access, while USDC is preferred for regulatory transparency and institutional use cases.

Most stablecoin transactions settle within seconds to minutes depending on the blockchain network used (e.g., Tron, Ethereum, or Solana).

Yes, in many jurisdictions they are legal, but they are regulated differently across countries. Compliance depends on local financial laws and frameworks like the GENIUS Act in the US.

The main risks include regulatory uncertainty, smart contract vulnerabilities, and reliance on centralized issuers for fiat-backed stablecoins.

They are already moving in that direction for cross-border and digital-native transactions, but full global standardization depends on regulation and institutional adoption.

Welcome to OwnProCrypto (Own & Pro Crypto) — a next-generation Bitcoin and blockchain education platform where the science of finance meets the power of AI-driven automation.

Our mission is simple: to equip you with the knowledge, frameworks, and tools needed to make smarter financial and business decisions in the Web3 economy.

Beyond analysis, OwnProCrypto focuses on transparency, verifiable data, and practical frameworks that investors and builders can actually use. Our goal is not hype — but clear thinking, disciplined analysis, and long-term value creation in the decentralized economy.

Our Background: Salim (Sam) is the founder and lead researcher behind OwnProCrypto, a Web3 intelligence platform focused on crypto security, digital ownership, stablecoin systems, interoperability, and institutional blockchain infrastructure.

Crypto Tools & Analysis:

Crypto Fundamental Analysis Tool | Protocol Evaluation System | DeFi Risk Analysis Tools | Crypto Portfolio Dashboard | Token Risk vs Reward Tool

Guides:

Crypto Fundamental Analysis | Blockchain Project Evaluation | Tokenomics Analysis | DeFi Protocol Analysis | Capital Efficiency

© 2026 OwnProCrypto — Built for smarter crypto decisions