Table of Contents

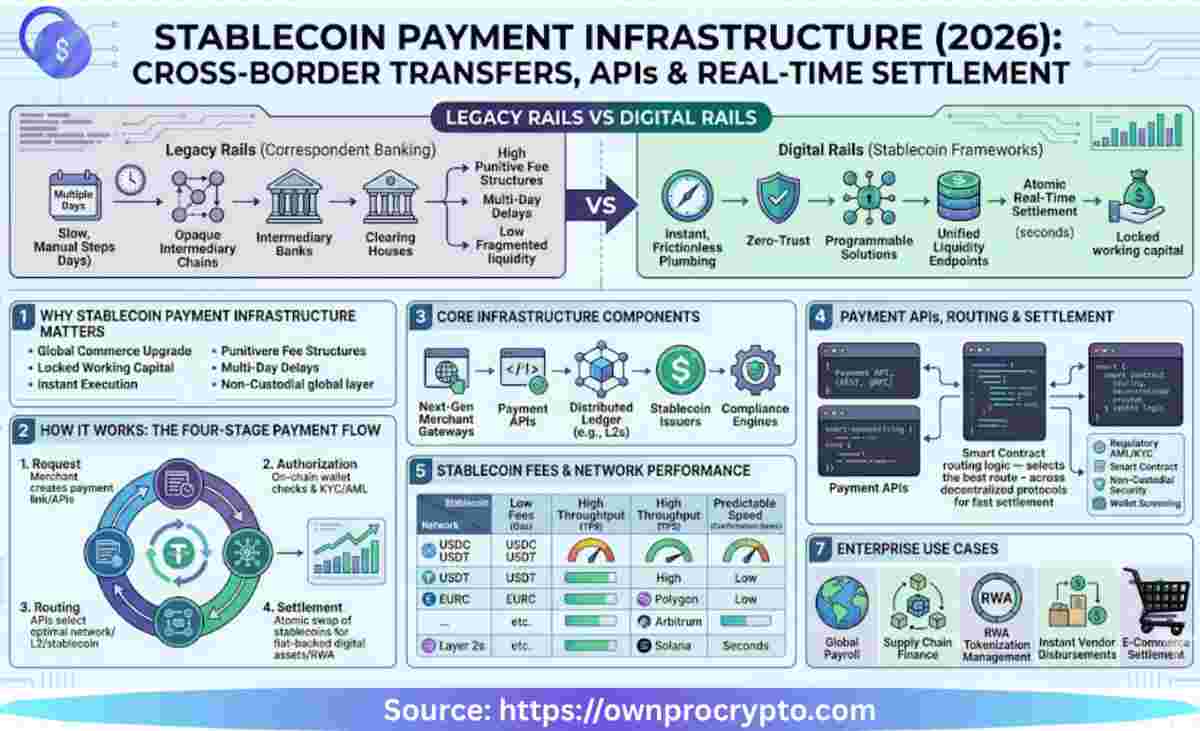

ToggleIn an era where legacy correspondent banking networks introduce multi-day delays and punitive fee structures, global commerce demands an absolute upgrade to instant, frictionless financial plumbing. Traditional cross-border channels remain the single greatest point of friction for international enterprises, leaving treasury departments restricted by fragmented liquidity and opaque intermediary chains. Fortunately, scalable blockchain frameworks have emerged to deliver zero-trust, programmable alternative solutions. This comprehensive guide covers Stablecoin Payment Infrastructure (2026): Cross-Border Transfers, APIs & Real-Time Settlement, unpacking how next-generation merchant gateways, unified liquidity endpoints, and institutional-grade payment APIs are routing around legacy vulnerabilities to establish a true real-time, non-custodial global settlement layer.

A real system isn’t just a wallet—it’s a stack of services working together:

This is what turns a simple transfer into a reliable financial operation.

Global payments remain dependent on systems originally designed decades ago.

Traditional cross-border payments often involve:

These processes create delays, increase costs, and reduce capital efficiency.

Stablecoin payment infrastructure offers an alternative model where value moves directly across blockchain networks with transparent settlement and continuous availability.

For enterprises, the opportunity is not simply faster payments. It is the ability to improve liquidity management, automate settlement workflows, and reduce operational friction.

Traditional Banking

Sender

│

▼

Bank A

│

▼

Correspondent Bank

│

▼

Clearing Network

│

▼

Bank B

│

▼

Recipient

Settlement Time:

2–5 Business DaysStablecoin Infrastructure

Sender

│

▼

Wallet

│

▼

Blockchain Network

│

▼

Recipient

Settlement Time:

Seconds to Minutes

At a high level, stablecoin payment infrastructure converts traditional fiat currency into digital assets, routes those assets across blockchain networks, and optionally converts them back into local currency.

The process relies on multiple systems working together rather than a single application.

Fiat Deposit

│

▼

Onramp Provider

│

▼

Stablecoin Issuance

│

▼

Blockchain Transfer

│

▼

Recipient Wallet

│

▼

Offramp Provider

│

▼

Bank SettlementA regulated provider receives fiat currency and issues an equivalent amount of stablecoins.

This creates the digital asset used for settlement.

The payment platform determines the most efficient route based on:

Modern routing engines automatically optimize these decisions.

The transaction is validated by the network and recorded on-chain.

Unlike traditional wires, there is no central clearing house involved.

Recipients can:

One of the largest advantages of stablecoin infrastructure is payment efficiency.

| Metric | Traditional Payments | Stablecoin Infrastructure |

|---|---|---|

| Settlement Time | 2–5 Days | Seconds to Minutes |

| Availability | Banking Hours | 24/7/365 |

| Intermediaries | Multiple | Minimal |

| Transparency | Limited | High |

| Reconciliation | Manual | Automated |

| Global Reach | High | Expanding |

| Cost Factor | Traditional Banking | Stablecoin Payments |

| Wire Fees | High | Low |

| FX Spreads | Significant | Often Lower |

| Intermediary Costs | Multiple Layers | Limited |

| Processing Costs | Variable | Predictable |

Legacy systems weren’t designed for real-time global commerce.

| Problem | Traditional Systems |

|---|---|

| Settlement Time | 2–5 days |

| Fees | 3–5% |

| Transparency | Low |

| Intermediaries | Multiple banks |

| Reversibility | Limited |

These inefficiencies create friction for freelancers, startups, and global businesses.

A stablecoin payment system consists of multiple layers.

Client

│

▼

API Gateway

│

▼

Payment Service

│

├──────► Compliance Layer

│

▼

Routing Engine

│

▼

Wallet Layer

│

▼

Blockchain Network

│

▼

Offramp Provider

│

▼

Bank Account

│

▼

Unified Ledger| Component | Purpose |

| API Gateway | Receives payment requests |

| Payment Engine | Executes transfers |

| Wallet Layer | Holds and manages funds |

| Compliance Layer | AML, sanctions, identity checks |

| Routing Engine | Network optimization |

| Onramp | Fiat-to-stablecoin conversion |

| Offramp | Stablecoin-to-fiat conversion |

| Ledger System | Reconciliation and reporting |

Modern payment platforms increasingly expose stablecoin functionality through APIs.

This allows businesses to automate:

The result is real-time settlement infrastructure that integrates directly into existing business systems.

| Step | Action |

| Input | $1,000 USD |

| Conversion | USD Stablecoin |

| Routing | Lowest-cost blockchain |

| Transfer | On-chain settlement |

| Offramp | Local conversion |

| Output | AED deposited locally |

| Metric | Result |

| Settlement Time | Under 5 Minutes |

| Fee Range | Low |

| Network | Solana, Stellar or Layer 2 |

| Visibility | Real-Time |

Different networks offer different trade-offs.

| Blockchain | Typical Cost | Speed | Primary Strength |

| Ethereum | Higher | Moderate | Liquidity |

| Solana | Low | Fast | Cost Efficiency |

| Stellar | Very Low | Fast | Payments |

| Layer 2 Networks | Low | Fast | Ethereum Compatibility |

Choosing the appropriate network depends on payment size, urgency, and liquidity requirements.

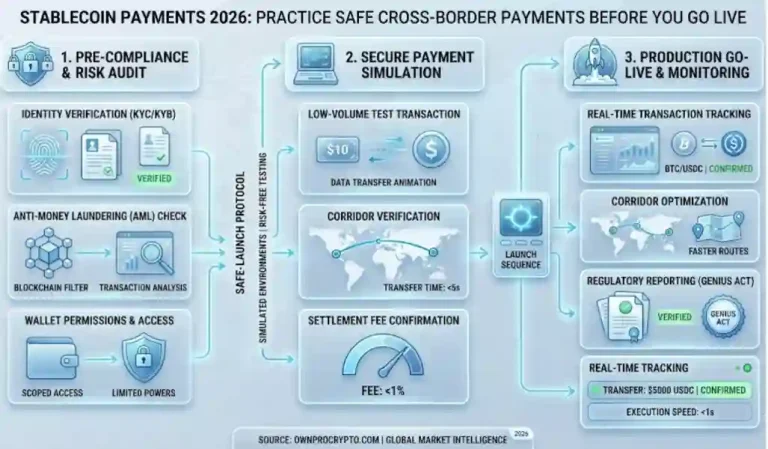

Fast settlement does not eliminate operational risk.

Strong controls remain essential.

| Risk | Potential Impact |

| Wrong Wallet Address | Irreversible Loss |

| Incorrect Network | Failed Transfers |

| Smart Contract Bugs | Asset Exposure |

| Compliance Failures | Regulatory Action |

| Liquidity Constraints | Settlement Delays |

| Control Area | Best Practice |

| Wallet Security | Multi-signature controls |

| Address Management | Whitelisting |

| Compliance | AML and KYC verification |

| Smart Contracts | Independent audits |

| Treasury Controls | Segregated custody |

| Monitoring | Real-time alerts |

Payment Request

│

▼

Identity Verification

│

▼

Compliance Screening

│

▼

Address Validation

│

▼

Approval Workflow

│

▼

Execution

│

▼

Settlement MonitoringSeveral industries are driving adoption. Enterprises achieve this by linking non-custodial payment gateways directly to their corporate balance sheet via real-time settlement APIs. Automated merchant infrastructure converts incoming client stablecoin transfers instantly into localized fiat or routes it straight into a secure, high-conviction Bitcoin treasury. This architecture eliminates legacy intermediary banking fees, ensures immediate capital efficiency, and allows organizations to manage dual-asset reserves cleanly on-chain.

Use stablecoin infrastructure to reduce payment delays and simplify international settlement.

Improve liquidity management and working capital efficiency.

Provide faster and lower-cost international transfers.

Integrate digital payment rails directly into customer products.

Several trends are shaping the next phase of growth:

Rather than replacing banks entirely, stablecoin infrastructure is increasingly becoming an additional settlement layer within modern financial systems.

The evolution of modern exchange demands more than just incremental speed; it requires an absolute overhaul of how value moves across borders. The integration of Stablecoin Payment Infrastructure (2026): Cross-Border Transfers, APIs & Real-Time Settlement marks a definitive shift away from legacy banking friction and toward instant, programmatic liquidity. By leveraging robust API architectures and zero-trust verification frameworks, institutional enterprises can now bypass intermediary delays, drastically optimizing capital efficiency and eliminating counterparty risk. the era of multi-day settlement windows and predatory cross-border fees is officially over. Embracing this real-time settlement infrastructure ensures that global corporate treasury operations remain fluid, compliant, and perfectly positioned for the next era of sovereign digital finance.

U.S. Treasury Digital Asset Report — Official insights into stablecoins, regulation, and the future of digital money. U.S. Treasury Digital Asset Report

To maintain topical clarity and avoid content overlap, this article should connect to a limited set of supporting authority hubs:

Each resource should address a distinct subject area while supporting a broader digital asset knowledge framework.

STABLECOIN PAYMENTS HUB

├── Foundations

├── Stablecoin Regulations (Exploring Now)

├── Stablecoins Are Now Insurable Money

├── Regulation & Trust

└── Stablecoins Are Now Insurable Money

├── Treasury & Institutions

├── Stablecoin Treasury Management

└── USDT Institutional Use Cases

└── Enterprise Adoption

Stablecoin payment infrastructure refers to the systems that enable digital asset payments, including wallets, APIs, compliance tools, routing engines, and settlement networks.

They can reduce settlement delays, improve transparency, and lower transaction costs.

Payment APIs allow businesses to automate transfers, treasury operations, and settlement workflows through software integrations.

Settlement speed depends on the network but is often measured in seconds or minutes rather than business days.

Security depends on wallet controls, smart contract audits, compliance systems, and operational governance.

Many organizations use stablecoins for liquidity management, supplier payments, and international settlement operations.

Overview

This Templates is designed for financial institutions, fintech companies, compliance teams, payment providers, regulators, digital asset businesses, treasury departments, and investors monitoring the evolution of stablecoins and Central Bank Digital Currencies (CBDCs).

This workbook provides a board-level and operational view of how stablecoins and CBDCs are transforming payments, compliance, treasury management, and financial infrastructure. It enables organizations to monitor regulatory obligations, manage risk, assess adoption trends, and prepare for the next generation of digital money ecosystems.

The framework focuses on:

Objective: Establish a comprehensive governance, compliance, and performance framework for stablecoin and CBDC activities in 2026 and beyond.

Maintain a master inventory of stablecoins used, accepted, or monitored.

| Stablecoin ID | Stablecoin Name | Symbol | Peg Type | Issuer | Status |

|---|---|---|---|---|---|

| SC001 | USD Stable | USDS | USD | Global Payments Ltd | Active |

| SC002 | Digital Dollar | DUSD | USD | Fintech Holdings | Active |

| SC003 | Euro Stable | EURS | EUR | Euro Finance Group | Active |

| SC004 | Asia Stable | ASDC | Basket | Asia Digital Bank | Pilot |

| SC005 | Treasury Coin | TUSDX | USD | Treasury Digital Corp | Active |

Track reserve backing and transparency.

| Stablecoin | Reserve Type | Reserve Coverage (%) | Latest Attestation Date | Independent Audit | Risk Rating |

|---|---|---|---|---|---|

| USDS | Cash & Treasuries | 102% | 15-May-2026 | Yes | Low |

| DUSD | Cash | 100% | 10-May-2026 | Yes | Low |

| EURS | Government Bonds | 101% | 20-Apr-2026 | Yes | Low |

| ASDC | Mixed Assets | 96% | 01-Apr-2026 | Partial | Medium |

| TUSDX | Cash & Treasuries | 104% | 05-May-2026 | Yes | Low |

Monitor payment activity and settlement performance.

| Transaction ID | Date | Stablecoin | Amount (USD) | Settlement Time | Status |

|---|---|---|---|---|---|

| TX1001 | 05-Jan-2026 | USDS | 12,500 | 8 sec | Completed |

| TX1002 | 18-Feb-2026 | DUSD | 45,000 | 10 sec | Completed |

| TX1003 | 10-Mar-2026 | EURS | 20,000 | 12 sec | Completed |

| TX1004 | 08-Apr-2026 | USDS | 75,000 | 9 sec | Completed |

| TX1005 | 22-May-2026 | TUSDX | 18,500 | 11 sec | Completed |

Track international stablecoin transfers.

| Transfer ID | Origin Country | Destination Country | Stablecoin Used | Amount | Compliance Status |

|---|---|---|---|---|---|

| CB001 | USA | Singapore | USDS | 50,000 | Approved |

| CB002 | Germany | UAE | EURS | 35,000 | Approved |

| CB003 | UK | India | DUSD | 25,000 | Approved |

| CB004 | Japan | Australia | USDS | 40,000 | Approved |

| CB005 | Canada | Brazil | TUSDX | 30,000 | Review Required |

Monitor suspicious activity and AML controls.

| Alert ID | Transaction ID | Alert Type | Risk Score | Investigation Status | Outcome |

|---|---|---|---|---|---|

| AML001 | TX1001 | Large Transfer | 25 | Closed | Cleared |

| AML002 | TX1002 | Velocity Alert | 45 | Closed | Cleared |

| AML003 | TX1003 | Jurisdiction Review | 60 | Open | Pending |

| AML004 | TX1004 | Pattern Analysis | 35 | Closed | Cleared |

| AML005 | TX1005 | High-Risk Counterparty | 80 | Investigating | Pending |

Track customer onboarding and verification.

| Customer ID | Customer Type | KYC Status | Last Review Date | Risk Classification | Compliance Status |

|---|---|---|---|---|---|

| C001 | Individual | Verified | 01-May-2026 | Low | Compliant |

| C002 | Business | Verified | 05-May-2026 | Medium | Compliant |

| C003 | Institution | Verified | 08-May-2026 | Low | Compliant |

| C004 | Individual | Pending | 12-May-2026 | Medium | Review Required |

| C005 | Business | Verified | 15-May-2026 | High | Enhanced Monitoring |

Measure compliance readiness against applicable regulations.

| Regulation Area | Requirement | Current Status | Compliance Score | Gap Identified | Action Owner |

|---|---|---|---|---|---|

| AML | Transaction Monitoring | Implemented | 95 | No | Compliance Team |

| KYC | Identity Verification | Implemented | 98 | No | Operations |

| Consumer Protection | Disclosure Controls | Partial | 80 | Yes | Legal Team |

| Reserve Reporting | Monthly Reporting | Implemented | 96 | No | Treasury |

| Data Privacy | User Data Protection | Implemented | 92 | Minor | IT Team |

Monitor CBDC initiatives and pilot projects.

| CBDC Program | Country | Pilot Phase | Participants | Launch Status | Readiness Score |

|---|---|---|---|---|---|

| Digital Dollar Pilot | USA | Testing | 50,000 | Pilot | 85 |

| Digital Euro Trial | EU | Advanced Pilot | 75,000 | Pilot | 88 |

| e-Rupee Program | India | Expansion | 120,000 | Active | 92 |

| Digital Yen Initiative | Japan | Pilot | 35,000 | Testing | 80 |

| Digital Real Program | Brazil | Expansion | 65,000 | Active | 90 |

Assess organizational preparedness for CBDC adoption.

| Assessment Area | Current Score | Target Score | Gap | Priority | Status |

|---|---|---|---|---|---|

| Technology Infrastructure | 85 | 95 | 10 | High | In Progress |

| Regulatory Readiness | 88 | 95 | 7 | Medium | On Track |

| Staff Training | 75 | 90 | 15 | High | Improvement Needed |

| Customer Education | 70 | 90 | 20 | High | Planned |

| Cybersecurity | 92 | 95 | 3 | Low | Strong |

Evaluate issuer and ecosystem risks.

| Counterparty | Category | Exposure Amount | Credit Assessment | Risk Rating | Monitoring Frequency |

|---|---|---|---|---|---|

| Global Payments Ltd | Issuer | 5,000,000 | Strong | Low | Monthly |

| Fintech Holdings | Issuer | 3,500,000 | Strong | Low | Monthly |

| Euro Finance Group | Issuer | 2,000,000 | Moderate | Medium | Monthly |

| Asia Digital Bank | Issuer | 1,000,000 | Moderate | Medium | Weekly |

| Treasury Digital Corp | Issuer | 4,500,000 | Strong | Low | Monthly |

Track growth and market acceptance.

| Metric | Q1 2026 | Q2 2026 | Q3 2026 | Q4 2026 Forecast | Trend |

|---|---|---|---|---|---|

| Active Wallets | 1.2M | 1.5M | 1.8M | 2.2M | Growing |

| Stablecoin Payments | $5B | $6.8B | $8.1B | $10B | Growing |

| CBDC Users | 400K | 650K | 900K | 1.4M | Growing |

| Merchant Adoption | 18% | 22% | 27% | 35% | Growing |

| Institutional Participation | 320 | 410 | 520 | 700 | Growing |

Maintain an audit trail of regulatory developments.

| Change ID | Effective Date | Jurisdiction | Regulatory Topic | Business Impact | Status |

|---|---|---|---|---|---|

| REG001 | 01-Jan-2026 | USA | Stablecoin Disclosure | Medium | Implemented |

| REG002 | 15-Feb-2026 | EU | Reserve Requirements | High | Implemented |

| REG003 | 01-Apr-2026 | Singapore | AML Updates | Medium | In Progress |

| REG004 | 01-Jun-2026 | UAE | Licensing Standards | High | Planned |

| REG005 | 01-Aug-2026 | UK | Consumer Protection | Medium | Planned |

Monitor operational liquidity supporting digital money activities.

| Treasury Asset | Balance | Liquidity Tier | Usage Purpose | Coverage Ratio | Status |

|---|---|---|---|---|---|

| Cash Reserves | 25,000,000 | Tier 1 | Redemptions | 105% | Healthy |

| Treasury Bills | 18,000,000 | Tier 1 | Reserve Backing | 102% | Healthy |

| Government Bonds | 12,000,000 | Tier 2 | Reserve Backing | 101% | Healthy |

| Bank Deposits | 8,500,000 | Tier 1 | Operations | 100% | Healthy |

| Emergency Fund | 5,000,000 | Tier 1 | Crisis Response | 110% | Strong |

Evaluate long-term strategic positioning.

| Strategic Area | Current Score | Target Score | Gap | Priority Level | Executive Owner |

|---|---|---|---|---|---|

| Stablecoin Readiness | 92 | 95 | 3 | Medium | COO |

| CBDC Integration | 80 | 95 | 15 | High | CTO |

| Regulatory Compliance | 94 | 98 | 4 | Medium | Chief Compliance Officer |

| Payment Innovation | 85 | 95 | 10 | High | Product Team |

| Global Expansion | 78 | 90 | 12 | High | Strategy Team |

Welcome to OwnProCrypto (Own & Pro Crypto) — a next-generation Bitcoin and blockchain education platform where the science of finance meets the power of AI-driven automation.

Our mission is simple: to equip you with the knowledge, frameworks, and tools needed to make smarter financial and business decisions in the Web3 economy.

Beyond analysis, OwnProCrypto focuses on transparency, verifiable data, and practical frameworks that investors and builders can actually use. Our goal is not hype — but clear thinking, disciplined analysis, and long-term value creation in the decentralized economy.

Our Background: Salim (Sam) is the founder and lead researcher behind OwnProCrypto, a Web3 intelligence platform focused on crypto security, digital ownership, stablecoin systems, interoperability, and institutional blockchain infrastructure.

Crypto Tools & Analysis:

Crypto Fundamental Analysis Tool | Protocol Evaluation System | DeFi Risk Analysis Tools | Crypto Portfolio Dashboard | Token Risk vs Reward Tool

Guides:

Crypto Fundamental Analysis | Blockchain Project Evaluation | Tokenomics Analysis | DeFi Protocol Analysis | Capital Efficiency

© 2026 OwnProCrypto — Built for smarter crypto decisions